What about Greece? What about it? - Corporates support lower longer volatility

What about Greece? What about it? - Corporates support lower longer volatilityTwo of the largest challenges now facing the world are Euro Sov and a large US slowdown. However, on the flip side, we have corporates with the highest cash levels in 25 years. In fact, they also have the best debt, interest and EBIT coverage on record. For any long vol trade to payoff exponentially, you need the market to “break” violently. This is hardly possible under a non-euro zone default. Corporates have de-levered and are benefiting from lower borrowing costs.

Let’s examine each scenario

1. Greece “ I don’t want to pay”

I don’t think anyone has edge in this situation, the spillover would be hard to contain and we could see large pensions wiped out and rampant speculation on who is next. Can we put a probability on this event happening? PFG would put it close to zero.

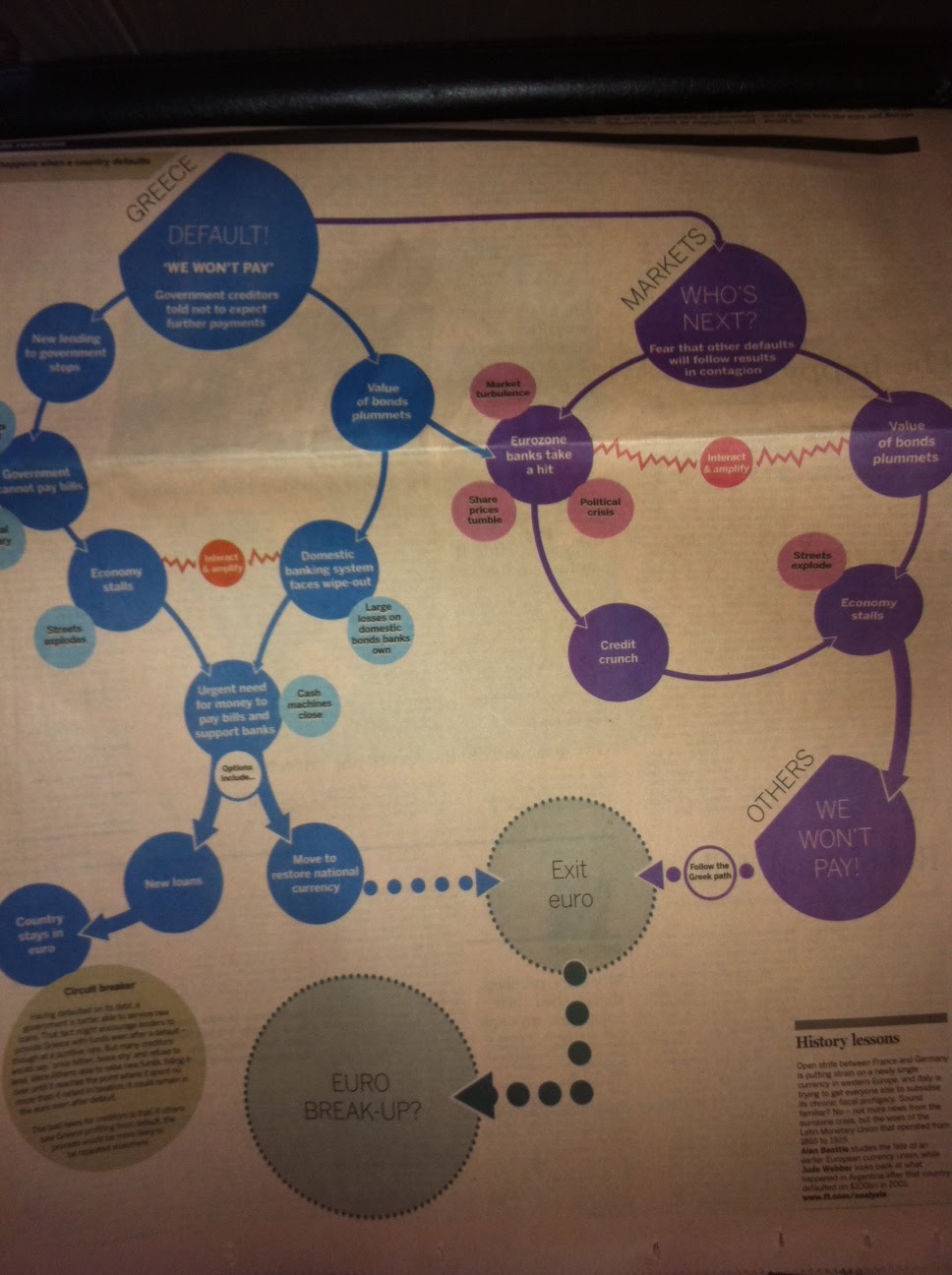

The FT has a great “what if” below. If the situation does occur, the world could easily say “I told you so” but I doubt we see a yawn, the global market in spite of being prepared for bankruptcy, would get rattled.

2. US Slowdown

Very real and PFG believes once the dust settles from Europe, the US jobs situation, the upcoming 2012 election will be the dominant stories moving the markets. The battle will continue of US Economics vs Corporate balance sheet health. PFG believes this will produce stale markets for a very long period, again supporting the case for lower long term volatility

In a picture

What could go wrong? CHINA. PFG believes that once the spotlight moves from Europe, it will start to shine on China and amplify many of the problems we see today. From being the global counter-party, lender and growth leader, China may have too much on it’s plate and a small reversal could send the global economy screaming for cover.

No comments:

Post a Comment