Obituary: Nov 30 2011, The Euro Died.

Obituary: Nov 30 2011, The Euro Died.As we posted yesterday, all risk-off indicators were at extremes and we got almost a 50 point rally in single day! Globally, everyone who had bet on the Euro to cease to exist won, it died. However, the trade was never to buy tails, cds or vix, it was simply to be long USD revenue balance sheets - i.e US Stocks. Why? As we saw today, trades betting a Euro diaster around the world woke up and vaporized quickly. The reason this happened is simple, the whole Earth just put on a massive short USD$ trade. You read that correct, the world is not flooded with dollars, however short USD as they are borrowing today with a promise to pay sometime in the future.

In accounting terms

-FED TRILLIONS USD

+ECB TRILLIONS USD

That leaves the future with every country who has been tapping these swap lines, short even more USD. When the time comes to pay, they will have to print their shit currency and buy ever expensive USD to return to the Fed. This move of course is exactly what the FED wants. They own the printing press which is the only way to cover your short.

So why US Balance Sheets?

The only way to have exposure/short cover a USD$ position is to own USD$ or own an asset that generates USD$. The Fed now has even more ability to print USD$ and they have created future demand for it. Global Balance sheets - ex USD simply cannot do that. They generate in local FX and borrow in USD. This is exactly why in a crisis, the world runs to USD$ as Global balance sheets debt side explodes with shrinking non dollar revenue.

How will this play out?

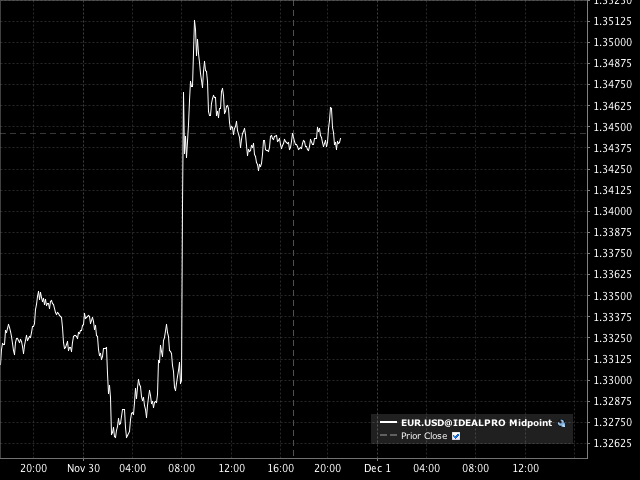

Well the death chart of the EUR after the announcement in fact looks exactly like a heart monitor of an ER patient shot in chest, one final gasp and then flat line.

Yes, we will have wild bond prints and wacky headlines, but the EUR IS DEAD.and betting on the Euro Zone implosion makes no sense as they have ample piles of unlimited USD available to fight whatever battle and don’t have to hide in the shame of IMF.

As we mentioned in our white paper early this year. Commodity prices are well bid and the problems will slowly begin to move to China now and why they suddenly needed to adjust the reserve ratio’s after 3 years? Expect demand for USD$ revenue assets to continue and more reports from Muddy Waters. Chanos on China will be the Paulson of Sub-Prime in 12 months. Not going to be a smooth ride.

No comments:

Post a Comment