Patience: Long Dated Vol will go down, the curve will flatten

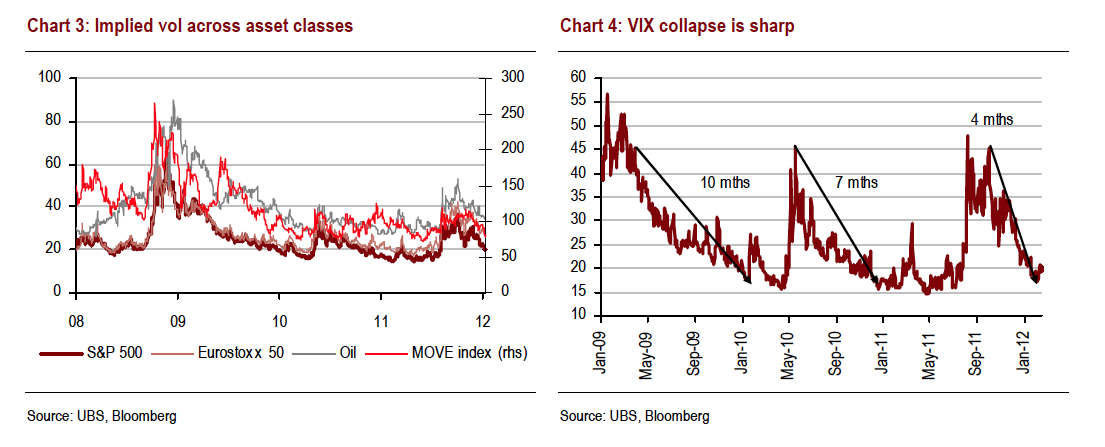

In all asset classes, we see the same thing, short dated vols are crushed as the market can’t seem to break out of this low correlation upward drift. It is the max pain path as everyone loaded up on short dated gamma as it “looks cheap”, except all it is doing is getting cheaper and causing option players to re-think continuously what delta they wish to hold against the cheap baby calls they are long. This is no easy matter, the upward drift pnl loss is real, the OTM call option gain is a combination of marks. Gamma and short dated vega is littered all over the street on dealer books. As nothing happens, it is being puked out to avoid paying anymore theta and we should get a move when they finally decide to get short it.

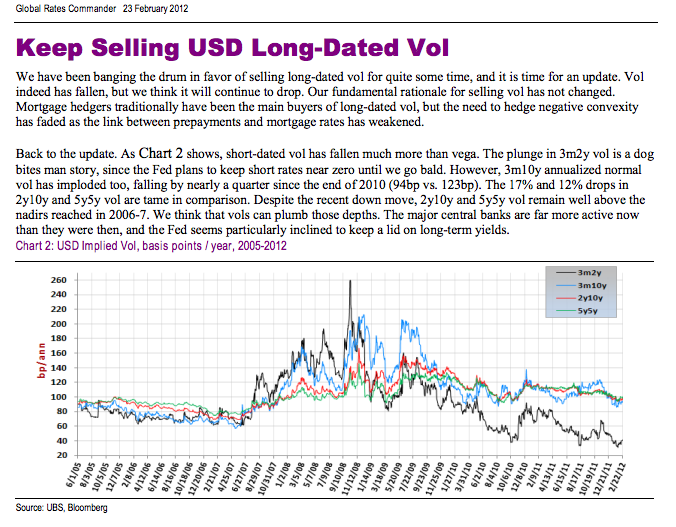

1. Interest Rate Vols

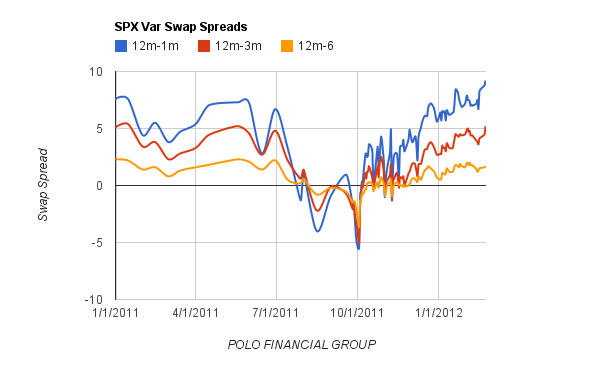

2. Recently steepness has picked up, giving long dated vol sellers a great entry point

3. Forward Vols Implied are also very high

4. Term Structure is also at extremes