Could we be entering a 2004-2007 low volatility world? All the graphs say yes, but you have to look a little further back in history, otherwise they are all screaming BUY

While everyone is focused on what will happen with Greece, specifically the March 2011 bond, the risk on world seems to have looked passed the drachma drama. Yes, we may have a few bumps along the way, but money is looking for a much riskier home these days

1. High Yield Spreads have come down really fast

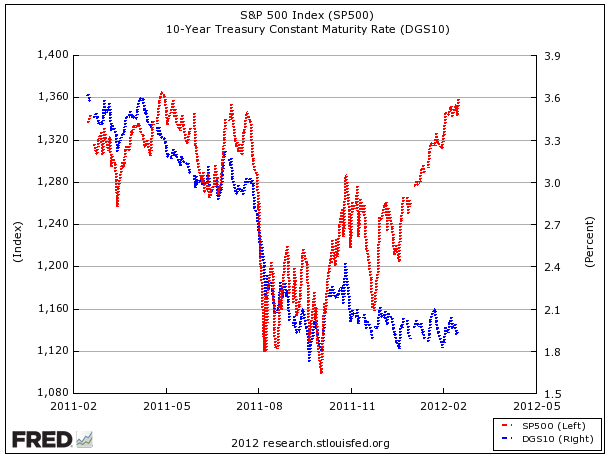

2. Large disconnect between credit and Equity - this is more due to the fed then natural forces to keep cheap money around for a long time

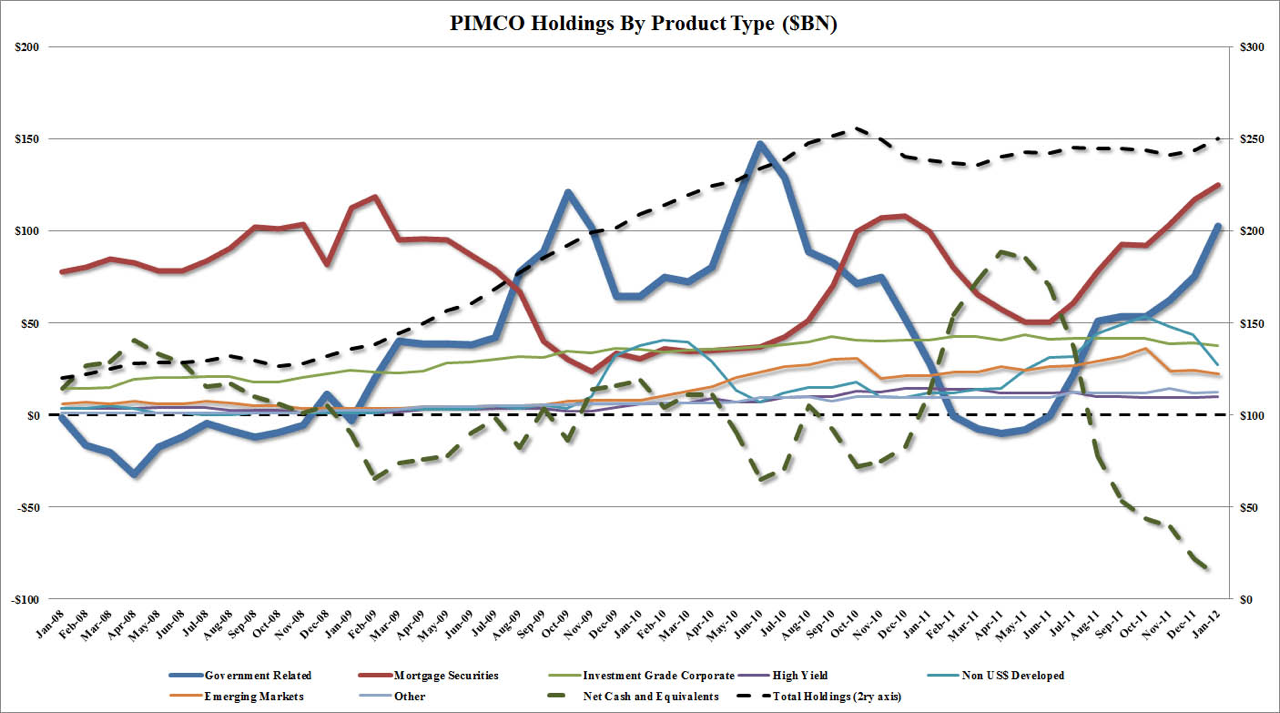

3. Even PIMCO’s Bill Gross has leveraged PIMCO to hold bonds and MBS. A full 180, but also viewed as short vol trade

4. Does anyone care about the Euro Danger? Vol has dropped really fast, skew however has not, currently in about the 85th percentile. Protection via tails is getting expensive again.

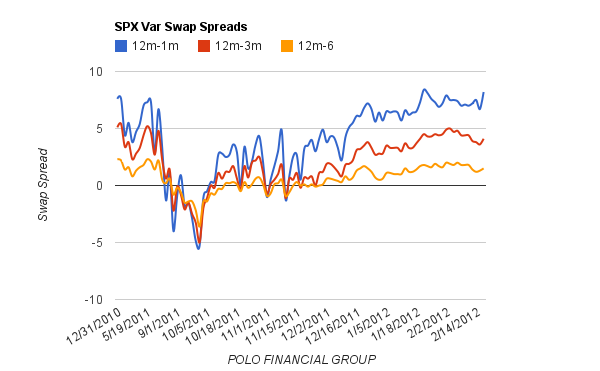

5. No demand for term structure for the front months. Record spreads over the last year. So why does no one “need” vol for anything imminent? Is the market simply trying to move vol demand forward and into lower strikes with Euro Bailouts?

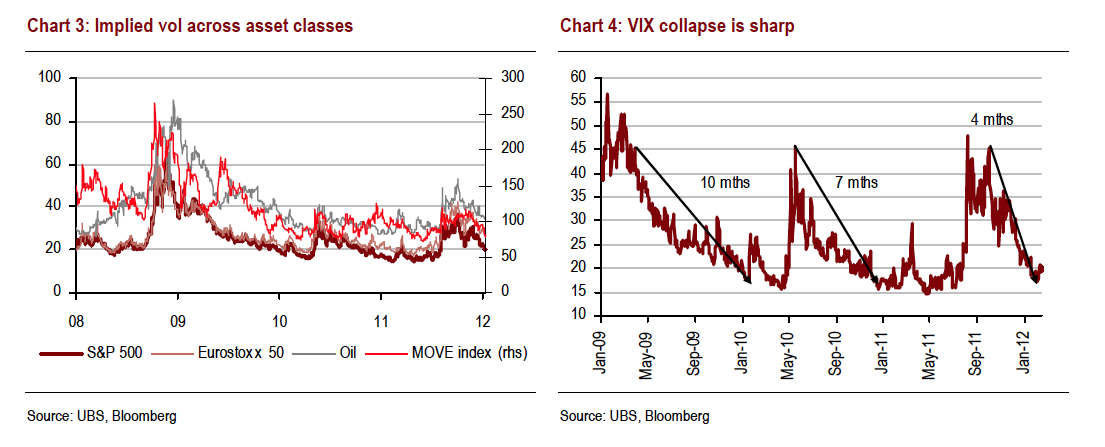

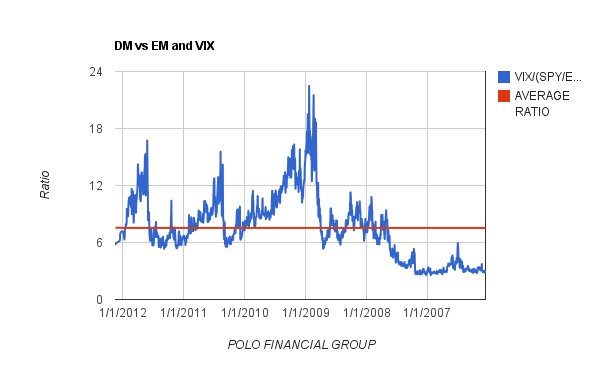

6. The risk EM/DM/VIX world also screaming to buy vol? But wait, look to your right and you can see that before all the Euro Drama, the 2004-2007 vol world, post Dot-Com and World Com, the vol markets did nothing for 3 years! and risk on was “ok”

7. Everything is saying buy vol if we just focus on the last 12 months? Is the risk on rally finally sending a message to the vol world that things are going to be fine?

8. According to UBS, global asset class vol viewed in a distribution format shows just have far vols have dropped. So this is not just a VIX story, in fact risk on this YTD is everywhere, except USTs, as the fed is keeping ZIRP 2014 and keeping the back -end kink in check to get people back into the housing trade (twist) - Remember this includes the risk-on in EUROPE, yields have fallen, buyers have shown up to buy bonds and European Banks stocks have boomed.

9. If we widen the horizon, look at post 2003, is post 2011 going to be the same?. Most people are looking at these graphs post 2008 and come up with “vol is cheap”

10. Interest Rate world sending same message - Long dated vol is to high and the story is the same, short dated vol smashed, long term vol has very little supply or courage to push it down.

We continue to believe that long term volatility is very overpriced, probably has a few suppliers and holding term-structure trades are the best way to position for the current environment. No one has any edge over the Euro headlines, as they flip-flop and shake people out of positions. However, we cannot ignore the massive flow into risky assets and markets making large bets that long term vol will go lower. Everyone is waiting for a “whale event” to feel better about selling vol, we are not sure they are going to get it or long vol holders will get the expected outcome.

No comments:

Post a Comment