YTD 2014 Short Vega investor letter. Also a look around the world using our Volatility XXX software

.png)

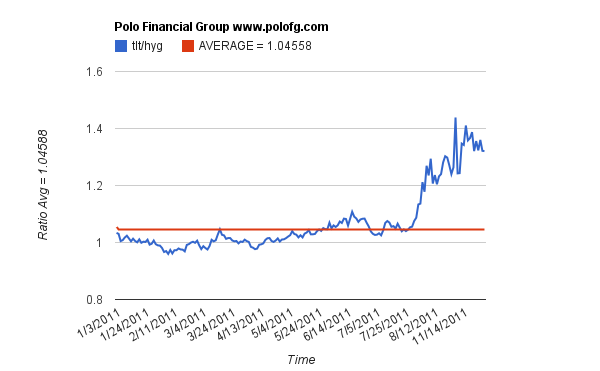

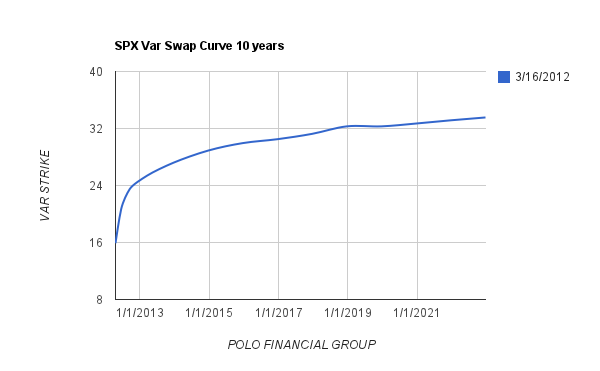

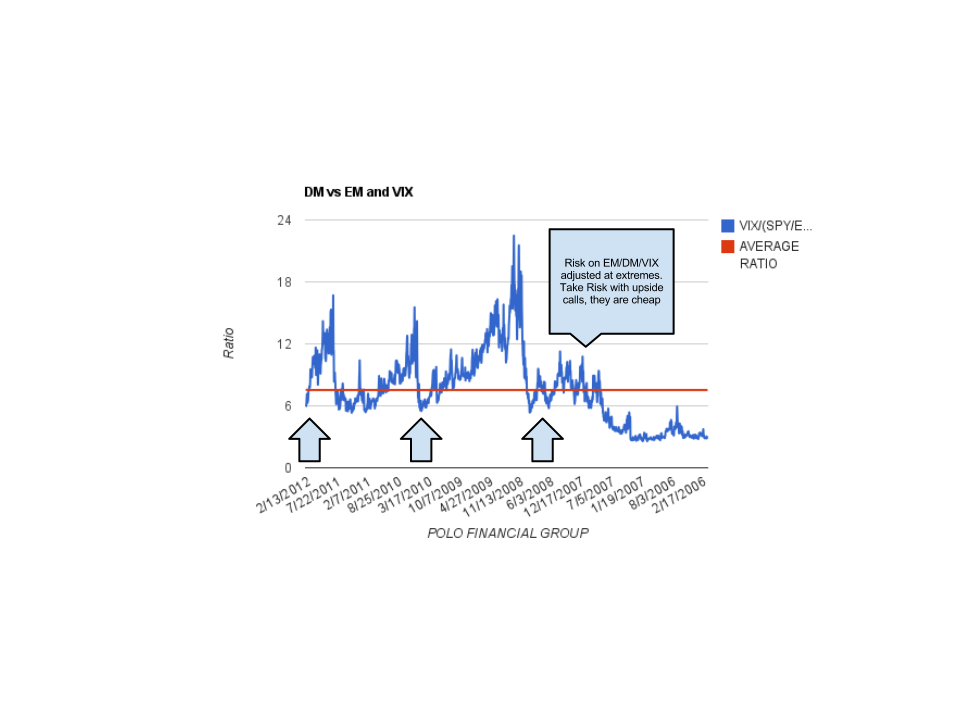

5. Vol traders are having fun playing the slide to take advantage of levered etf flows and perpetual fear in the market

5. Vol traders are having fun playing the slide to take advantage of levered etf flows and perpetual fear in the market

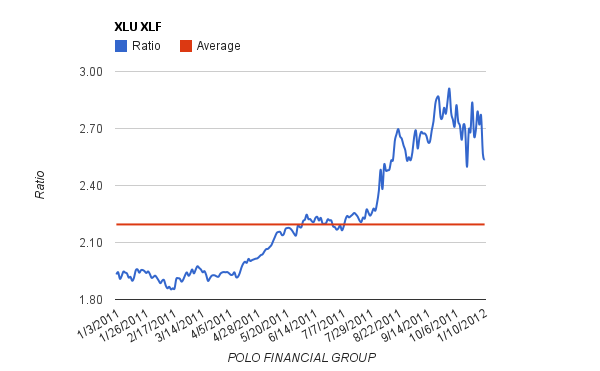

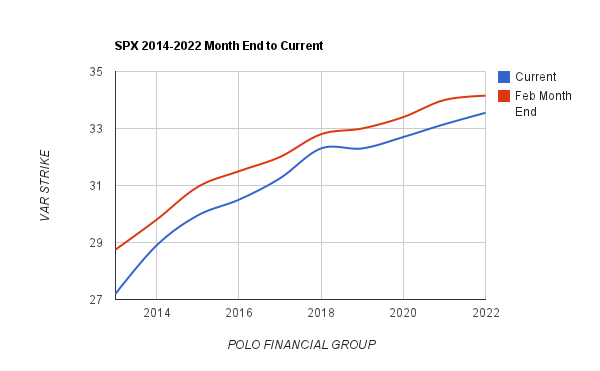

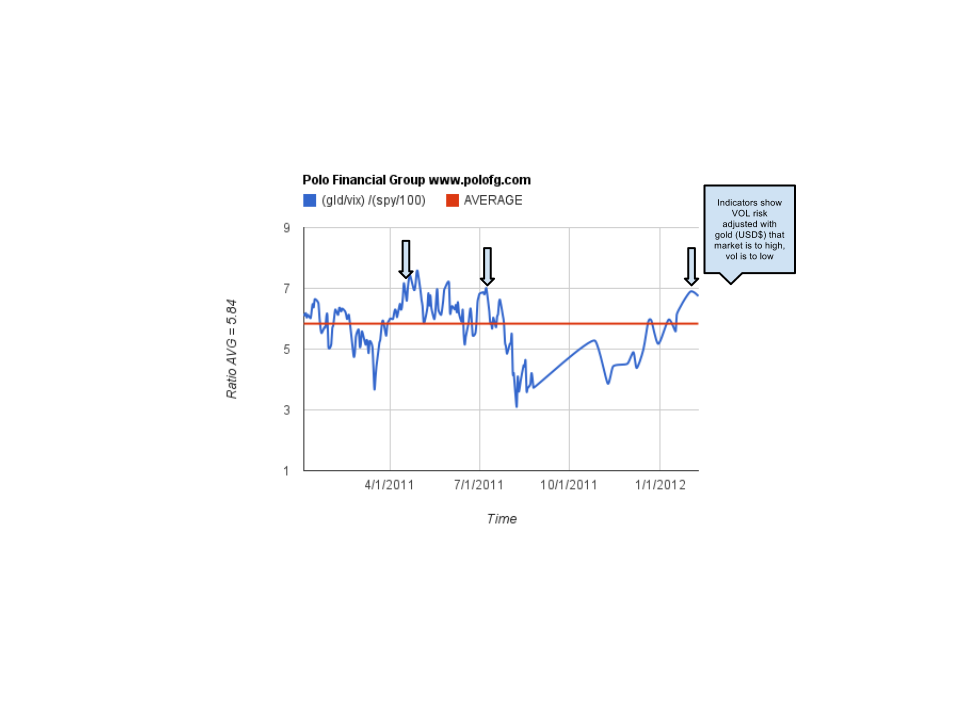

Still plenty of upside left.

Still plenty of upside left.

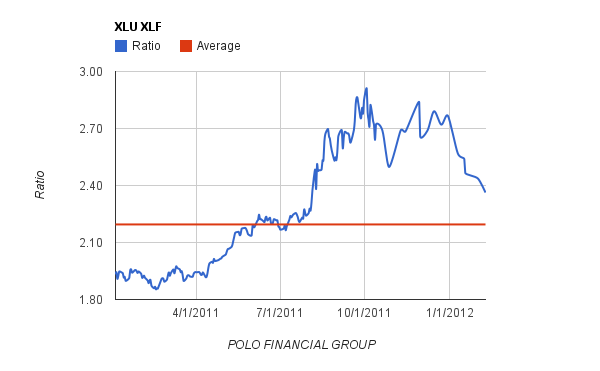

| Fund Changes by 1/3 | YTD Performance |

| XFN/XLU | 14% |

| EEM/SPX | 7.5% |

| Long/Short | 5.3% |

| Bond | 2.7% |